79Likes

79Likes LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks

may be I am wrong but I think that SSA is recalculating (same as repainting) ...Originally Posted by zilliq

This is a discussion on AllAverages within the Trading tools forums, part of the Trading Forum category; Originally Posted by zilliq Another idea for the next version, Do you think it's possible to add the SSA of ...

may be I am wrong but I think that SSA is recalculating (same as repainting) ...

Thanks newdigital,

Do you think that all ssa recalculating/repainting ?

If so, it isn't necessary to include it in the next version

Zilliq

I am not very sure but as far as I remember - all the versions of SSA are recalculated (by 2 bars back, or 10 bars back - based on the settings in indicator)

all are except the normalized end pointed versions... and then they are not as pretty and "perfect"...

Hi Igor,

An idea for the next 3.2 version : Add the nonlagMA 7.2 (you are the author right ?)

Have a nice day

Zilliq

Hi Igorad,

Plase can you post the formula of the correct version of the T3 (mode 24) (not the original), because I would code it on prorealtime

Thanks a lot and have a nice week-end

Zilliq

Hi Zilliq,

Do you have any version of the T3 for prorealtime? If yes then please use following formula for the T3 length:

len = (period + 5.0)/3.0-1;

if len < 1 then len = 1;

where period - input parameter.

Regards,

Igor

Thanks igorad,

Just to be sure, you replace period by

len=((period+5)/3)-1 or len=(period+5)/(3-1) ? (I think it's the first answer, but just to be sure

The code I use on prorealtime for the T3 is

price= customclose

x1=(exponentialaverage[period](price))*(1+vfactor)

x2=(exponentialaverage[period](exponentialaverage[period](price)))*vfactor

gd=x1-x2

x11=(exponentialaverage[period](gd))*(1+vfactor)

x21=(exponentialaverage[period](exponentialaverage[period](gd)))*vfactor

gd1=x11-x21

x12=(exponentialaverage[period](gd1))*(1+vfactor)

x22=(exponentialaverage[period](exponentialaverage[period](gd1)))*vfactor

gd2=x12-x22

Where period is the lengh on my code

So, the difference is only on the lengh with this "correct" version ?

Thanks a lot

Zilliq

The code on Prorealtime would be:

price= customclose

len = ((period + 5.0)/3)-1

if len < 1 then

len = 1

endif

vfactor=0.7

x1=(exponentialaverage[len](price))*(1+vfactor)

x2=(exponentialaverage[len](exponentialaverage[len](price)))*vfactor

gd=x1-x2

x11=(exponentialaverage[len](gd))*(1+vfactor)

x21=(exponentialaverage[len](exponentialaverage[len](gd)))*vfactor

gd1=x11-x21

x12=(exponentialaverage[len](gd1))*(1+vfactor)

x22=(exponentialaverage[len](exponentialaverage[len](gd1)))*vfactor

gd2=x12-x22

return gd2 as "T3 correct Tillson"

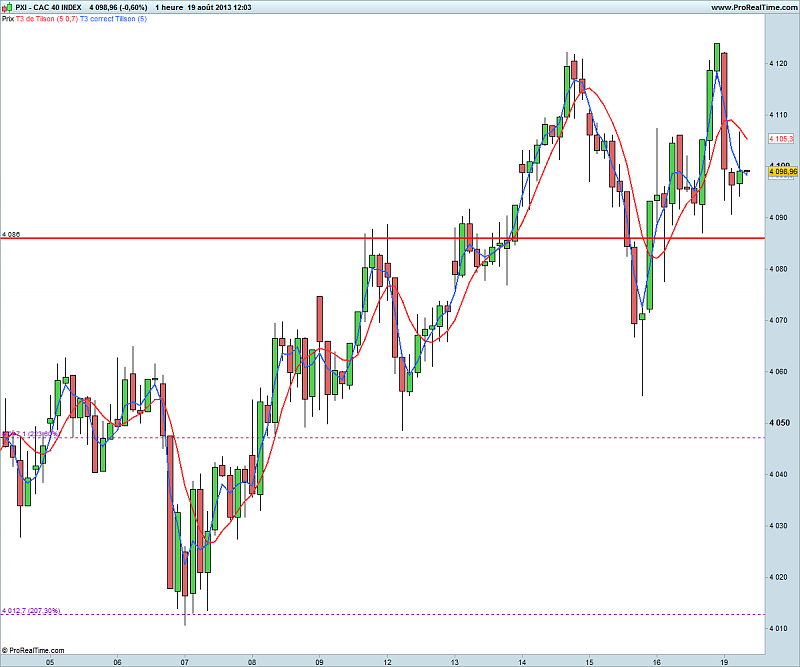

And here is the difference with period=5

In blue the "correct Tillson", and in red the "original Tillson"

The correct is faster but less smoother

Could you confirm the post above

Thanks a lot

Zilliq (coder on Prorealtime)

And if it isn't secret can you post the formula of the JSmooth because we haven't such a moving average on Prorealtime and I would code it for the community. Thanks a lot

Last edited by zilliq; 08-19-2013 at 10:10 AM.

Hi Zilliq,

Answers on your questions:

1. the 1st formula is OK.

2. I see issues in your code, because I guess the function exponentialaverage allows to enter only integer value for the EMA period. So you should allow to enter double values in this function.

3. About JSmooth:

Did you see the code for TradeStation? If not then please use following code for the JSmooth:

Regards,Code:{******************************************************************* Description : Jurik Smoothing Provided By : TrendLaboratory(c) Copyright 2008 Author : IgorAD E-mail: igorad2003@yahoo.co.uk ********************************************************************} Inputs: Price(NumericSeries), Period(NumericSimple), Pow(NumericSimple), Phase(NumericSimple), Opt(NumericSimple); Vars : bet(0.45*(Period-1)/(0.45*(Period-1)+2)),Filt0(0),alpha(0),Det0(0),Filt1(0),Det1(0),Filt2(0); If CurrentBar = Period then begin Filt0 = Price; Filt1 = Price; Filt2 = Price; end else begin alpha = power(bet,Pow); Filt0 = (1-alpha)*Price + alpha*Filt0[1]; Det0 = (Price - Filt0)*(1 - bet) + bet*Det0[1]; Filt1 = Filt0 + Phase*Det0; Det1 = (Filt1 - Filt2[1]) * power((1 - alpha),2) + alpha*alpha*Det1[1]; Filt2 = Filt2[1] + Det1; if Opt = 0 then JSmooth = Filt0; if Opt = 1 then JSmooth = Filt1; if Opt = 2 then JSmooth = Filt2; end;

Igor

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote

Bookmarks