LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks

Date: 12th July 2024.

Market News The Aftermaths of Inflation.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

* Treasuries surged after a much cooler than expected CPI report that saw Fed funds futures price in a -25 bp rate cut for September, more than 2 quarter point moves over the rest of the year, and 3 cuts by the end of Q1 2025.

* Australian and New Zealand government bonds rallied, taking cues from their US counterparts.

* European stocks open muted, following a sharp decline in Asian equities driven by a significant drop in technology stocks. Despite this recent downturn, global stocks are on track for their 6th consecutive weekly gain, the longest streak since March, buoyed by expectations of Fed easing which have supported overall risk sentiment.

Asian & European Open:

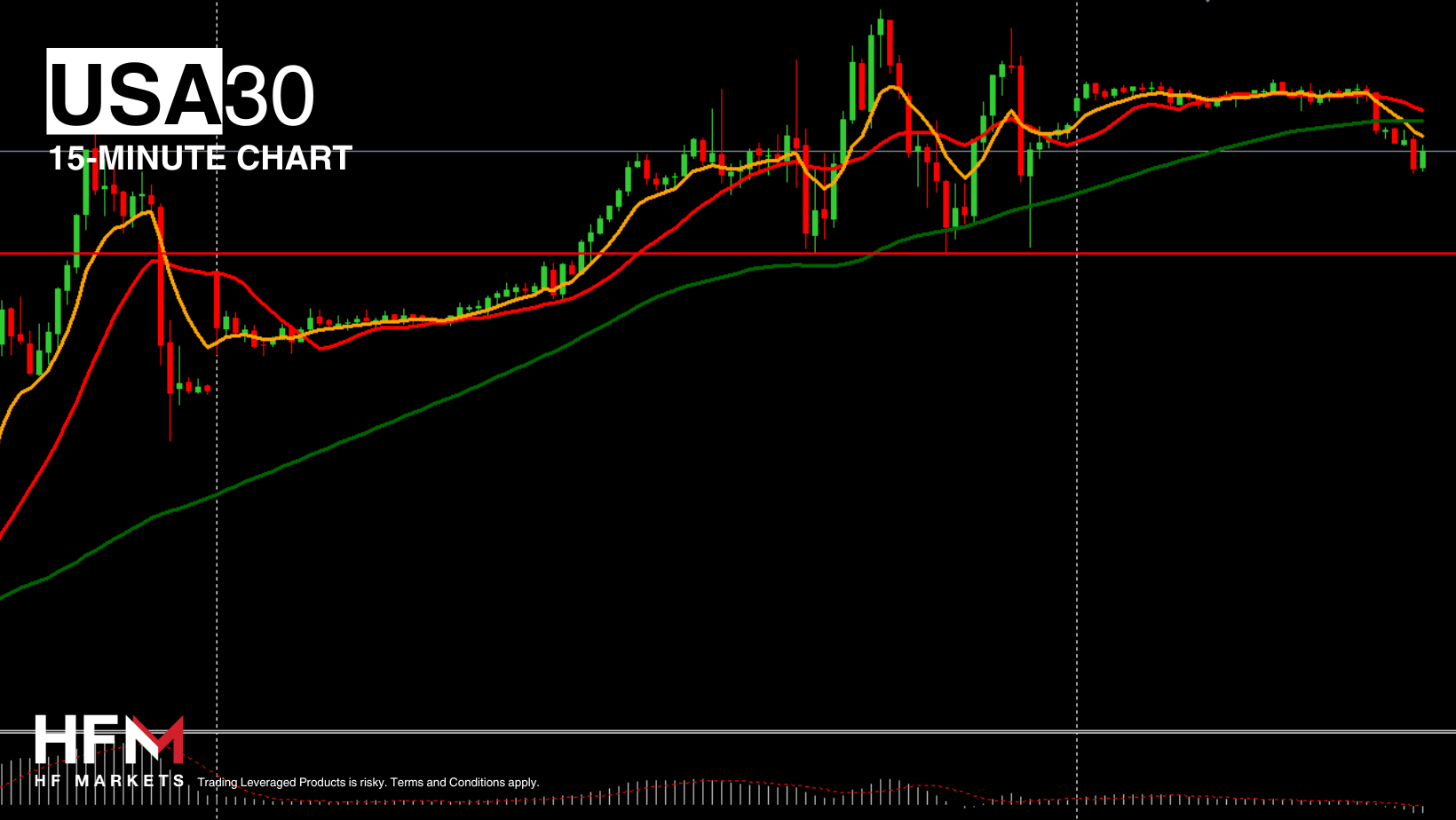

* Wall Street was not as enthused, although its coming off of prior strong gains. The NASDAQ slumped -1.95% and the S&P500 slid -0.88% to 5584. Cash fled some of the safety of the mag 7. The Dow was up 0.08%.

* Disappointing earnings from Delta and PepsiCo weighed heavily.

* The Euro Stoxx 50 futures showed minimal change, mirroring the stability seen in US stock futures after a tech-driven selloff on Thursday.

Financial Markets Performance:

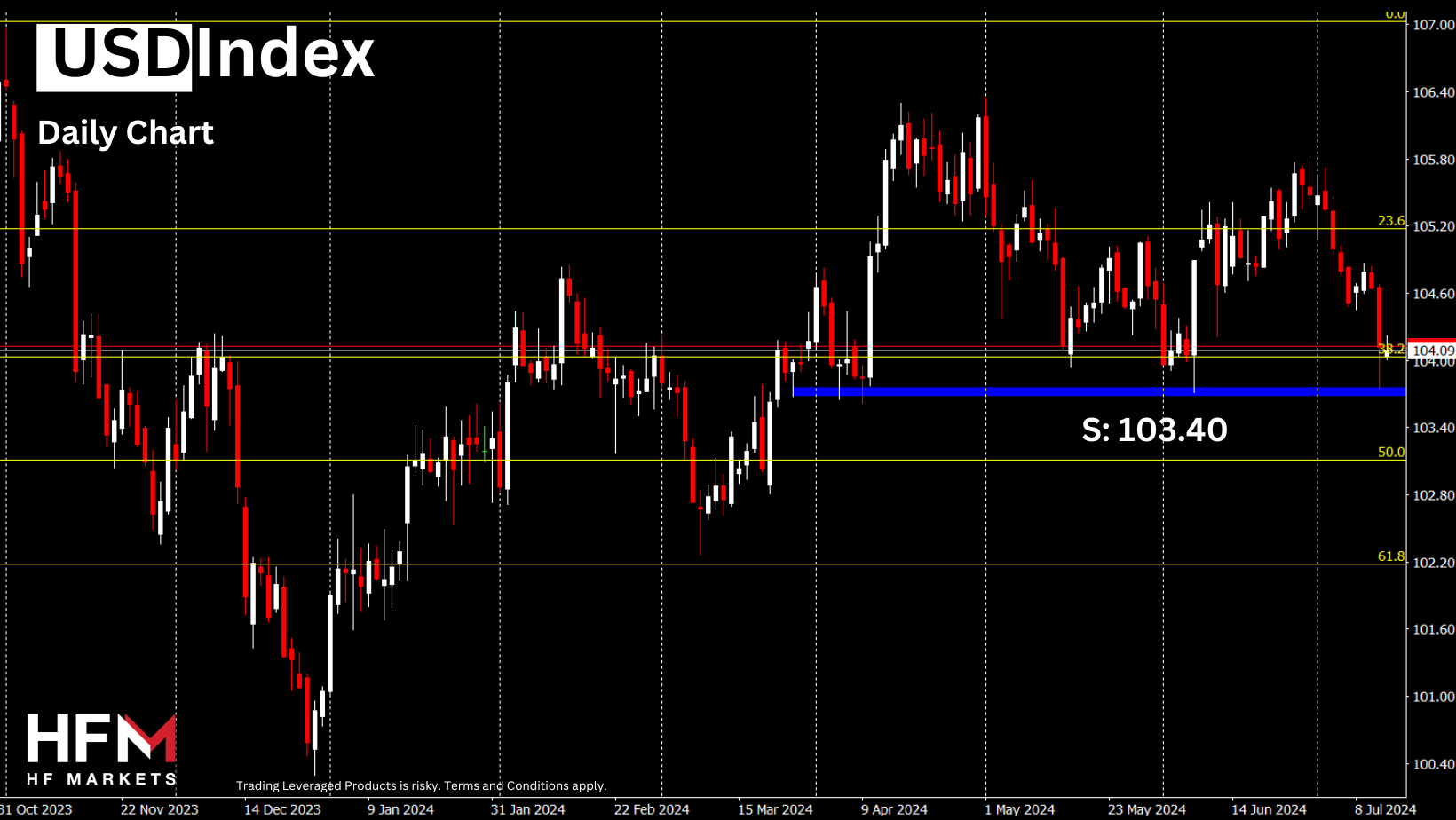

* The USDIndex took it on the chin, falling to 104.07 from the high of 104.99 on the dovish Fed outlook.

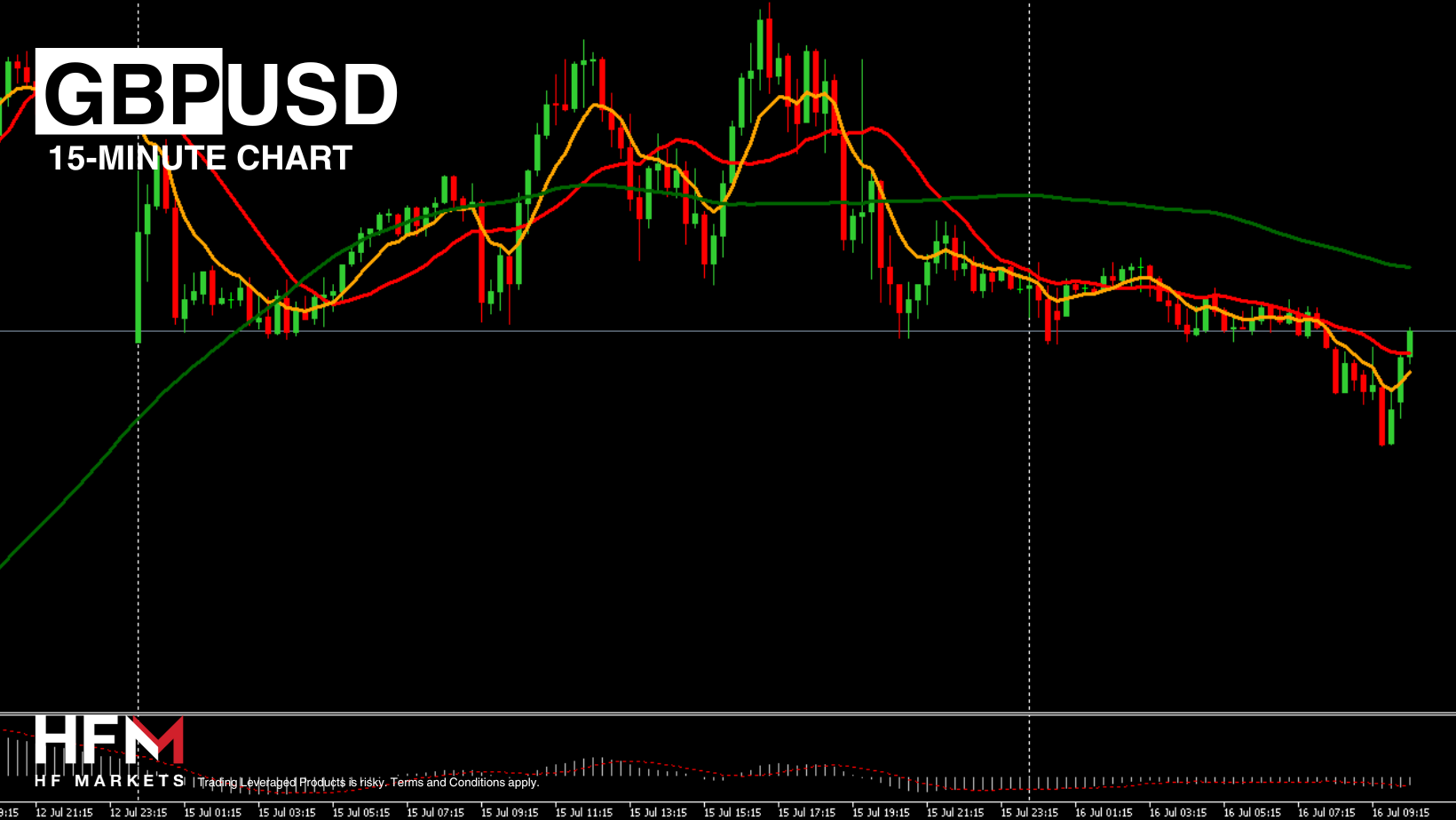

* A lot of the weakness came from JPY as USDJPY crashed 4-handles, as there were reports of intervention. The Bank of Japan conducted rate checks with traders, reinforcing the belief that authorities had intervened in the market on Thursday to support the currency.

* Oil prices rallied for a 3rd day in a row boosted by the US inflation which cooled broadly in June to the slowest pace since 2021. Bets rose that the Fed will start to reduce borrowing costs this quarter.

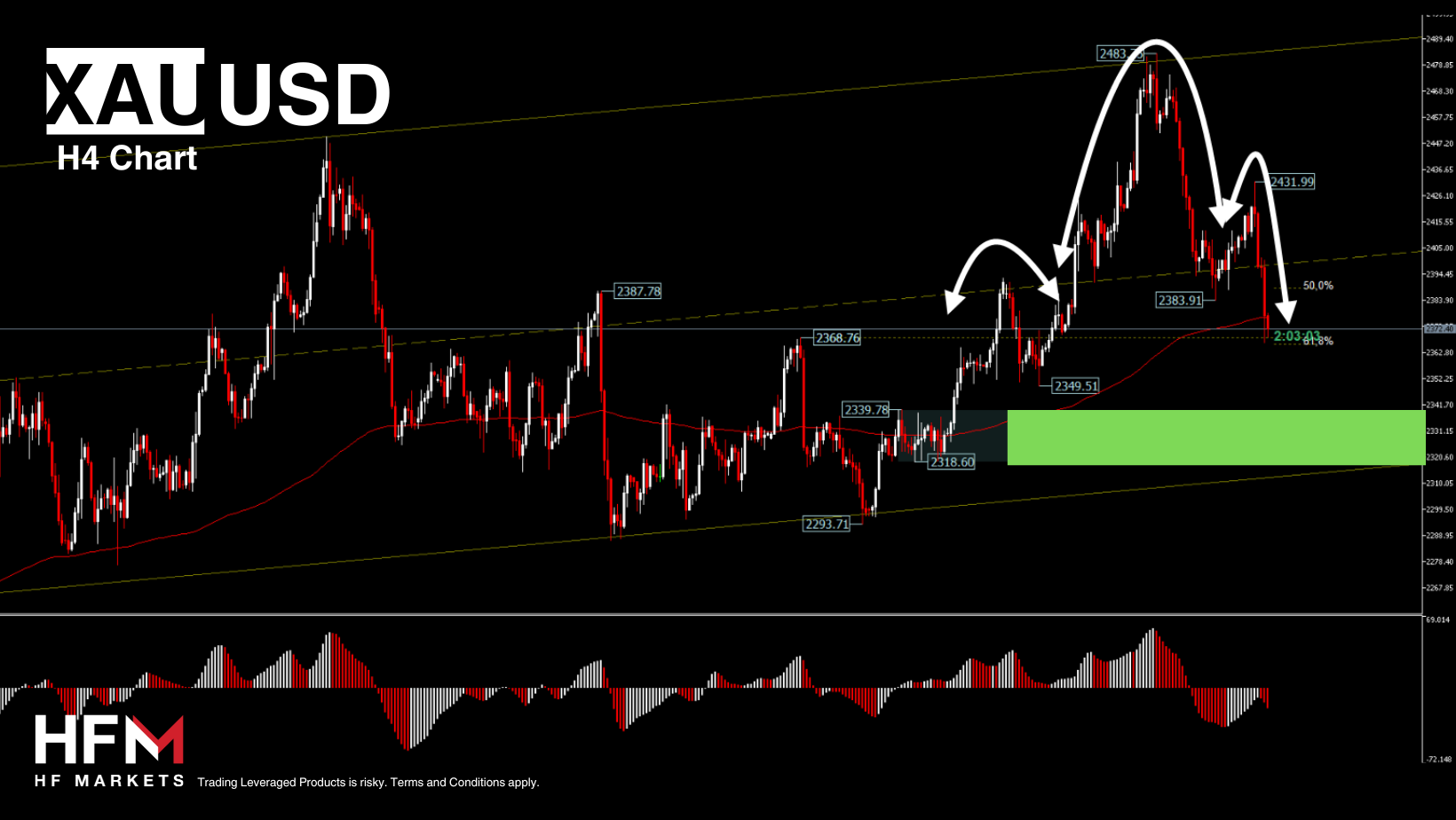

* Gold corrects some of yesterdays gains, back to 2400.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Reply With Quote

Reply With Quote

Bookmarks