3Likes

3Likes LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks

Date : 20th December 2022.

Market Update December 20 Pre-Christmas Surprise from BOJ.

Trading Leveraged Products is risky

*The USD Index is betwixt and between amid various drivers. It closed at 104.706, inside the days 104.931 to 103.50 range. The advent of the holidays and year end have lightened volume measurably too, exacerbating some of the moves in the markets. Stocks are in red against Decembers seasonality. Treasuries fell today, especially at longer tenors, after the Bank of Japan unexpectedly lifted a cap on 10-year yields and unleashed a sell-off across global bond markets.

*Yields: 10yr rose to 3.71% and 30-yr to 3.72%.

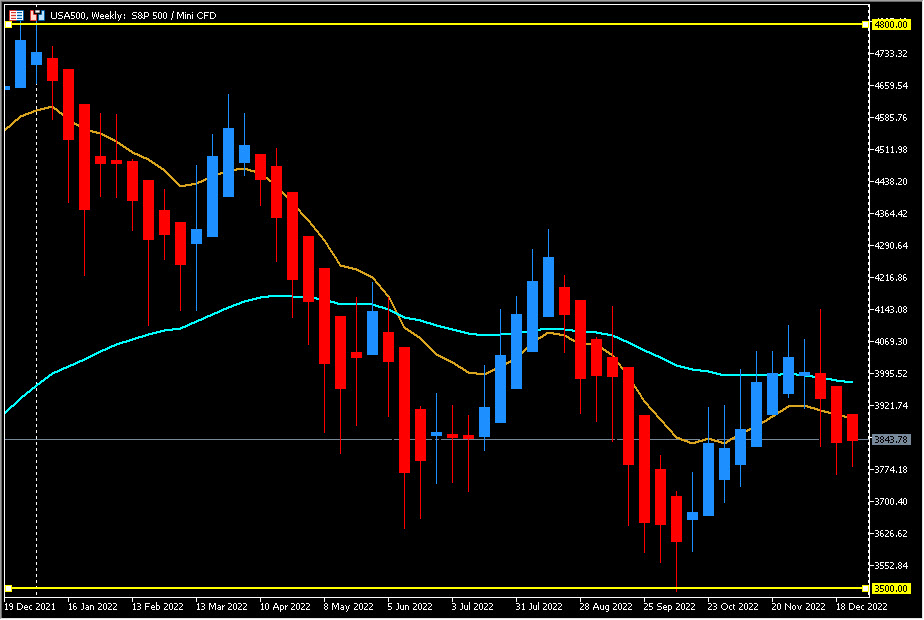

*The S&P 500 has risen in 73% of December since 1928, according to Dow Jones Market Data. As of Mondays close, the S&P 500 had fallen 6.4% in December.

*EUR tumbling between 1.0575-1.0650.

*JPY surged to 132.66 after the BOJ said it would review its yield curve control policy and widened the trading band for the 10-year government bond yield in an unexpected tweak. (Policy is unchanged)

*AUD & NZD drifted also after BOJ announcement.

*Stocks The NASDAQ tumbled -1.49%, with the S&P 500 falling -0.90%, while the Dow slid -0.49%. Nikkei closed with a -2.5% loss.

*SUSOil drifts to $75.20 from $76.55.

*SGold higher but still struggling to break the $1,800.

*SBTC retested again the $16,200 floor. Sam Bankman-Fried to agree to US extradition after Bahamas court hearing.

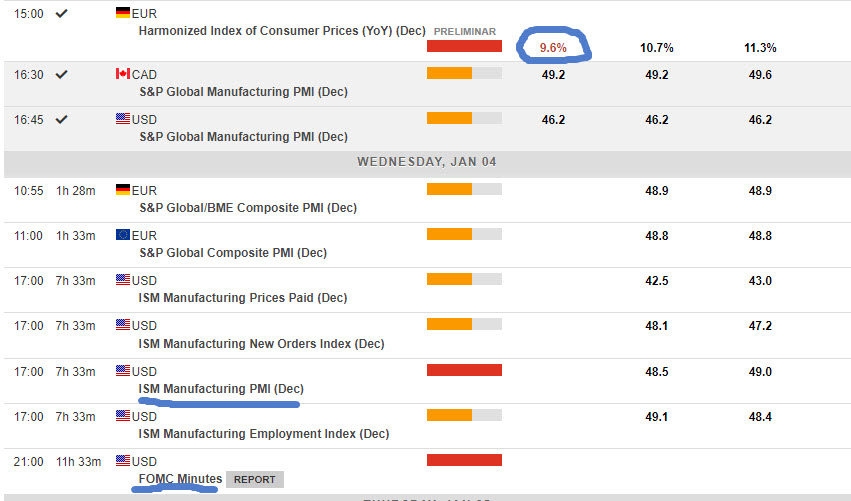

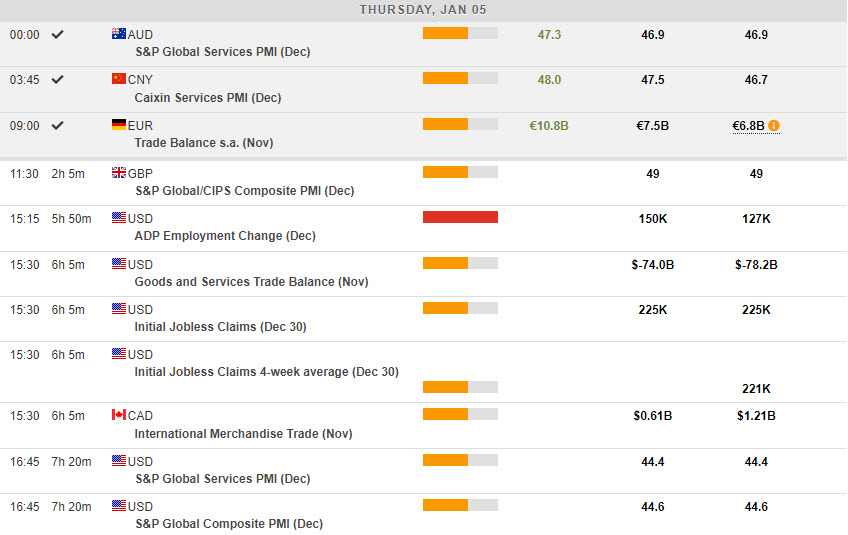

Today US Housing Starts & Building Permits, Canadian Retail Sales, EU Consumer Confidence and NZ Trade data.

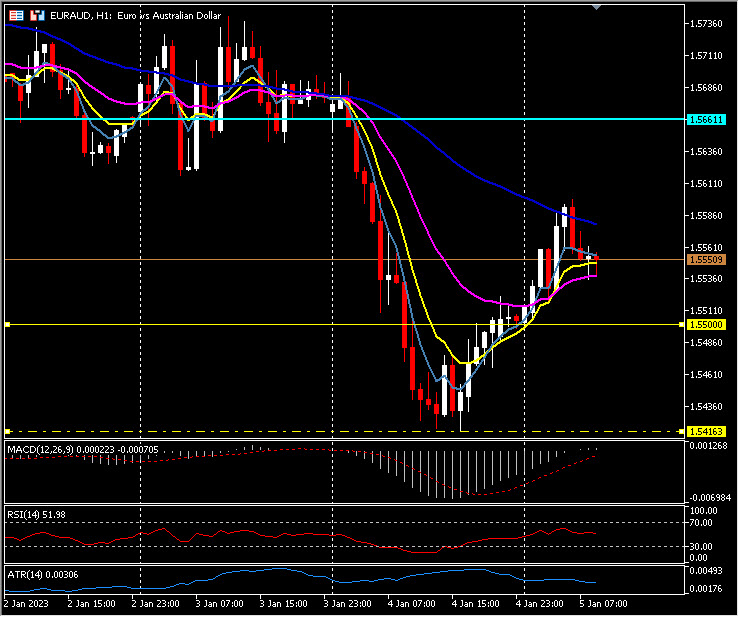

Biggest FX Mover@ (07:30 GMT) AUDJPY (-3.32%). Broke 8-month support extending to 88.30, below 50-week EMA. Intraday MAs keep pointing lower, MACD histogram & signal line negative and falling. RSI 22 & flat, H1 ATR 0.4920, Daily ATR 1.1611.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Andria Pichidi

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Reply With Quote

Reply With Quote

Bookmarks