3Likes

3Likes LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks

Date : 15th September 2022.

Market Update September 15 USD Holds at Highs, Stocks Flat.

Trading Leveraged Products is risky

*USDIndex Remains bid and back to test 109.85. US Mortgages over 6%, (Highest since 2008), 2/30yr. yields most inverted since 2000. 2/10s 45 pts inverted. INFLATION the only story in town. Key next week will be the Feds new forecasts, and especially the dot plot and what it suggests about the terminal rate. Fed funds futures point to about a 4.4% rate in early spring.

*EUR Trades at 0.9964 now and remains capped by Parity 1.0000 resistance. Lane yesterday suggested that another 75 bp rate hike is not a done deal. EU is looking for $140 billion for Winter Energy support.

*JPY BOJ intervention not imminent. Katayama: Japan lacks effective means to combat Yens sharp falls . USDJPY back to 143.75, 145.00 remains vital resistance.

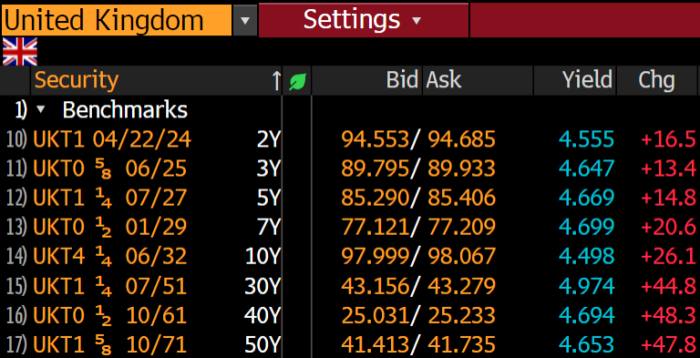

*GBP back to key 1.1500 support zone now, having rejected 1.1600 yesterday.

*Stocks US stocks held at lows and remain subdued after Tuesdays bloodbath.(S&P500 +0.34% 13pts 3946) FUTS trade at 3965. Starbucks +5.53%, TSLA +3.59%. NASDAQ best performer (+0.74%) Asian stock markets also weak and European FUTS also flat.

*USOil topped at $90.00 yesterday and trades at $88.30 now. 20-day moving average sits at $89.00.

*Gold remains anchored under $1700 trades at key $1688 now.

*BTC slumped to $19.5k but holds at $20k now. Ethereum PARIS Merge successful this morning.

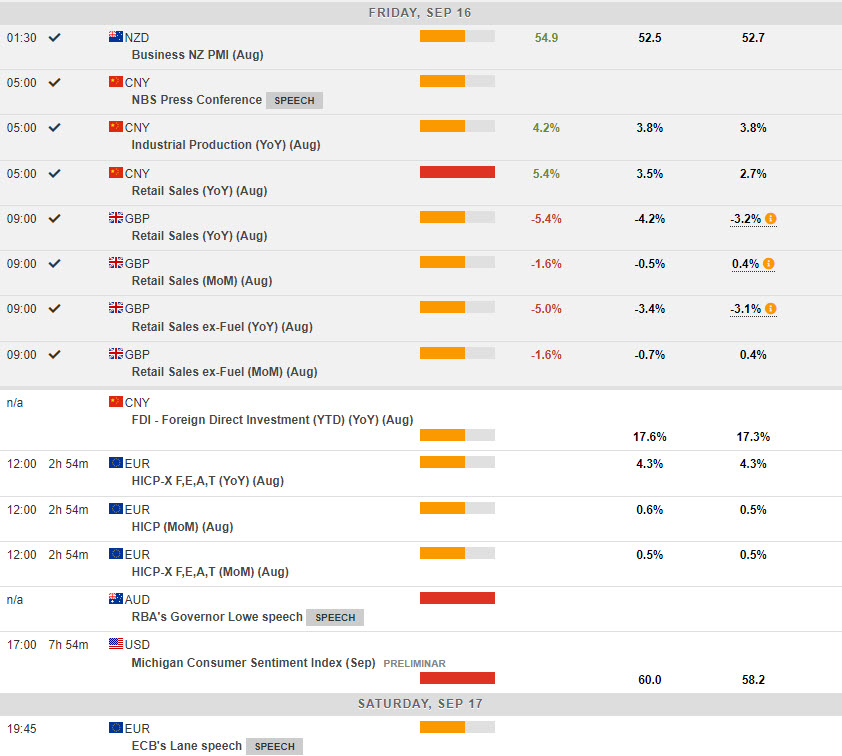

Overnight & Today US Philly Fed, US Retail Sales, Speech from ECBs de Guindos.

Biggest FX Mover @ (06:30 GMT) USDJPY (+0.39%) The BOJ intervention gossip & weak data not aiding the YEN yet. Rallied from 142.50 lows yesterday to 143.70 now 145.00 remains key resistance. MAs aligning higher, MACD histogram & signal line negative but rising, RSI 57.50, H1 ATR 0.227, Daily ATR 1.632.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Reply With Quote

Reply With Quote

Bookmarks